The flat-panel display market has long been marked by a series of peaks and valleys, and a new report by market research firm DSCC says a downturn may be on the way.

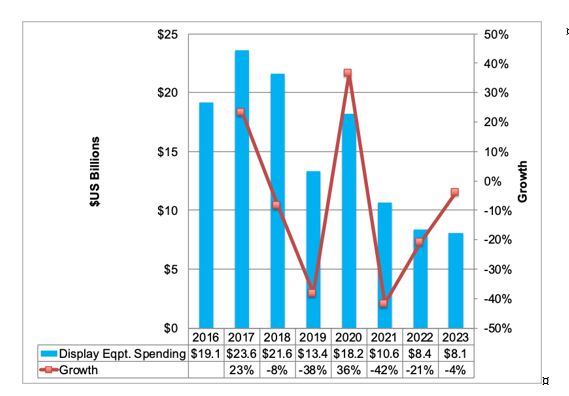

According to the firm, in 2018 display equipment spending fell 8 percent to $21.6 billion, the second highest result in the history of the display industry. OLED fab spending fell 7 percent, while LCD fab spending fell 10 percent, with OLEDs accounting for a 58 percent share. China dominated spending with a 92 percent, with the top five equipment suppliers for 2018 were AMAT, Canon, Nikon, Tokyo Electron and ULVAC.

DSCC is projecting a 38 percent decline in capex for 2019, to $13.4 billion, which the firm attributes to fab delays resulting from weakening market conditions, funding challenges or other issues. LCD fab spending is expected to be down 9 percent year-to-year, with OLED spending down 59 percent, worsened by poor mobile OLED fab utilization. The figure shows projected display capital expenditures for 2019 and beyond.

LCDs are projected to account for 61 percent of spending in 2019, with China is expected to maintain a 92 percent share. DSCC expects the 2019 fab delays to lessen the impact of the oversupply of large-area display panels, thus leading to slower price reductions and better returns for display companies.

Looking further ahead, DSCC expects display capital expenditures to rise 36 percent in 2020 to $18.2 billion, the fourth highest spending total in the history of the display industry. OLED spending is expected to rebound, rising 111% with LCDs down 10 percent. 2020 will mark the first time OLEDs will dominate display expenditures, accounting for a 60 percent share.

The report also addresses ten different next-generation TV technology alternatives which could slow down production decisions in the 2021-2024 period adding to the uncertainty in this period and potentially creating shortages. DSCC is currently predicting just 2 percent year-over-year growth in capacity in 2022 and 2023, as a result of conversions to more process-intensive technologies as well as delays in placing bets on next-generation technologies until they mature.